Linear Mean-Reversion Strategies for Portfolio Trading

In Example we determined that the EWA-EWC-IGE portfolio formed with the “best” eigenvector from the Johansen test has a short half-life. We can now confidently proceed to backtest our simple linear mean-reverting strategy on this portfolio. The idea is the same as before when we own a number of units in USD.CAD proportional to their negative normalized deviation from its moving average (i.e., its Z-Score). Here, we also accumulate units of the portfolio proportional to the negative Z-Score of the “unit” portfolio’s price. A unit portfolio is one with shares determined by the Johansen eigenvector. The share price of a unit portfolio is like the share price of a mutual fund or ETF: it is the same as its market value. When a unit portfolio has only a long and a short position in two instruments, it is usually called a spread.

Note that by a “linear” strategy we mean only that the number of units invested is proportional to the Z-Score, not that the market value of our investment is proportional.

This linear mean-reverting strategy is obviously not a practical strategy, at least in its simplest version, as we do not know the maximum capital required.

Example: Backtesting a Linear Mean-Reverting Strategy on a Portfolio

The yport is a Tx1 array representing the net market value of the “unit” portfolio calculated in the preceding code fragment. num Units is a Tx1 array representing the multiples of this unit portfolio we wish to purchase. (The multiple is a negative number if we wish to short the unit portfolio.) All other variables are as previously calculated. The positions is a Tx3 array representing the position (market value) of each ETF in the portfolio we have invested in.

(This code fragment is part of cointegrationTests.m.)

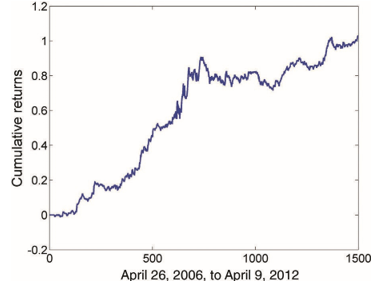

Figure. displays the cumulative returns curve of this linear mean reverting strategy for a stationary portfolio of EWA, EWC, and IGE.

FIGURE. Cumulative Returns of a Linear Trading Strategy on EWA-EWC-IGE Stationary Portfolio

We find that APR = 12.6 percent with a Sharpe ratio of 1.4 for the strategy.

At the outset and we cannot really enter and exit an infinitesimal number of shares whenever the price moves by an infinitesimal amount. Despite such impracticalities, the importance of backtesting a mean-reverting price series with this simple linear strategy is that it shows we can extract profits without any data-snooping bias, as the strategy has no parameters to optimize. (Remember that even the look-back is set equal to the half-life, a quantity that depends on the properties of the price series itself, not our specific trading strategy.) Also, as the strategy continuously enters and exits positions, it is likely to have more statistical significance than any other trading strategies that have more complicated and selective entry and exit rules.

Pros and Cons of Mean-Reverting Strategies

It is often fairly easy to construct mean-reverting strategies because we are not limited to trading instruments that are intrinsically stationary. We can pick and choose from a great variety of cointegrating stocks and ETFs to create our own stationary, mean-reverting portfolio. The fact that every year there are new ETFs created that may be just marginally different from existing ones certainly helps our cause, too.

Besides the plethora of choices, there is often a good fundamental story behind a mean-reverting pair. Why does EWA cointegrate with EWC? That’s because both the Canadian and the Australian economies are dominated by commodities. Why does GDX cointegrate with GLD? That’s because the value of gold-mining companies is very much based on the value of gold. Even when a cointegrating pair falls apart (stops cointegrating), we can often still understand the reason. For example, as we explain in next blog, the reason GDX and GLD fell apart around the early part of 2008 was high energy prices, which caused mining gold to be abnormally expensive. We hope that with understanding comes remedy. This availability of fundamental reasoning is in contrast to many momentum strategies whose only justification is that there are investors who are slower than we are in reacting to the news. More bluntly, we must believe there are greater fools out there. But those fools do eventually catch up to us, and the momentum strategy in question may just stop working without explanation one day.

Another advantage of mean-reverting strategies is that they span a great variety of time scales. At one extreme, market-making strategies rely on prices that mean-revert in a matter of seconds. At the other extreme, fundamental investors invest in undervalued stocks for years and patiently wait for their prices to revert to their “fair” value. The short end of the time scale is particularly beneficial to traders like ourselves, since a short time scale means a higher number of trades per year, which in turn translates to higher statistical confidence and higher Sharpe ratio for our backtest and live trading, and ultimately higher compounded return of our strategy.

Unfortunately, it is because of the seemingly high consistency of mean reverting strategy that may lead to its eventual downfall. As Michael Dever pointed out, this high consistency often lulls traders into overconfidence and overleverage as a result (Dever, 2011). (Think Long Term Capital Management.) When a mean-reverting strategy suddenly breaks down, perhaps because of a fundamental reason that is discernible only in hindsight, it often occurs when we are trading it at maximum leverage after an unbroken string of successes. So the rare loss is often very painful and sometimes catastrophic. Hence, risk management for mean reverting is particularly important, and particularly difficult since the usual stop losses cannot be logically deployed. I discuss why this is the case, as well as techniques for risk management that are suitable for mean reverting strategies.

Read Also; Johansen Cointegration Test Explained for Algorithmic Trading Strategies